This week, the total inventory of construction steel continued to decline. Specifically, the total rebar inventory decreased by 1.82% WoW, while the total wire rod inventory increased by 0.68% WoW. On the supply side, the operating rates of both BF and EAF steel mills declined this week. Currently, due to reduced profitability, steel mills in Shaanxi have halted production for maintenance, leading to a decrease in pig iron production.

The production situation of EAF steel mills has diverged. In east China, one EAF mill has resumed production. In the southwest region, due to electricity subsidies, market profitability has recovered, prompting some EAF mills to extend their operating hours. In south China, due to rainy weather and difficulties in collecting steel scrap, overall profitability has been poor, leading some EAF mills with severe losses to halt production for maintenance. On the demand side, driven by the speculation surrounding the "coal essay" and the consecutive days of steel price declines, downstream procurement enthusiasm has increased, and overall transaction volumes have improved. Consequently, the total inventory of construction materials has continued to decline this week.

This week, the total rebar inventory stood at 5.3786 million mt, a decrease of 99,600 mt WoW, or a 1.82% decline (previous value: -3.66%). Compared to the same period of the lunar calendar last year, it decreased by 1.9139 million mt, or a 26.24% decline (previous value: -24.25%).

Table 1: Overview of Rebar Inventory

Data source: SMM

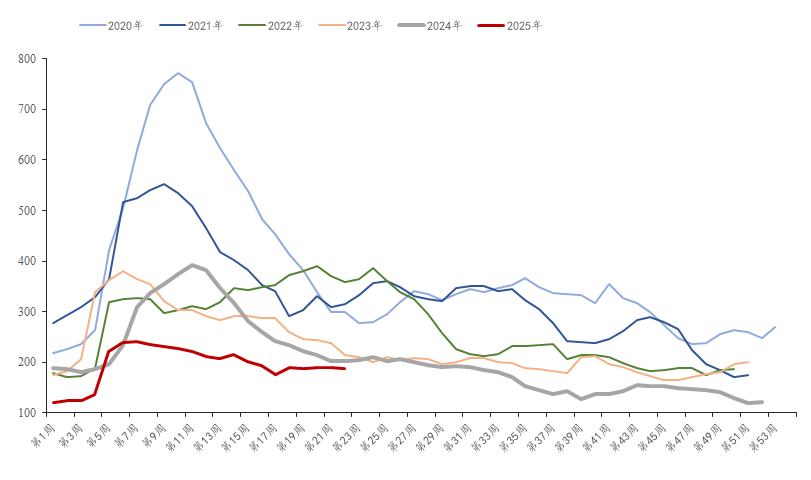

This week, the in-plant inventory of rebar was 1.8813 million mt, a decrease of 16,900 mt WoW, or a 0.89% decline (previous value: -0.31%). Compared to the same period last year, it decreased by 224,000 mt, or a 10.64% YoY decline (previous value: -7.4%). This week, the operating rates of both BF and EAF steel mills declined, leading to a decrease in overall supply levels. Additionally, the current direct supply situation of steel mills is favorable, resulting in a decrease in in-plant inventory of construction materials.

Chart-1: Overview of Rebar Factory Inventory Trends from 2020 to 2025

Data source: SMM

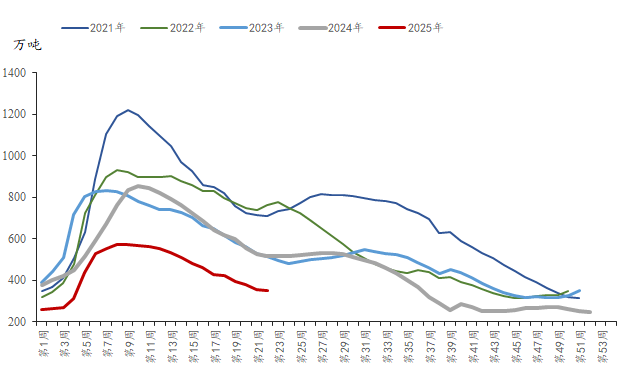

This week, the social inventory of rebar was 3.4973 million mt, a decrease of 82,700 mt WoW, or a 2.31% decline (previous value: -5.35%). Compared to the same period last year, it decreased by 1.6899 million mt, or a 32.58% YoY decline (previous value: -30.92%). The market fluctuations triggered by the "coal essay" speculation have become a focal point, stimulating the ferrous metals series futures to fluctuate upward. Coupled with the consecutive days of steel price declines, the market trading atmosphere has improved, and overall transaction volumes have surged. Consequently, the social inventory has continued to decline this week.

Chart-2: Overview of Rebar Social Inventory Trends from 2021 to 2025

Data source: SMM

Overall, this week, the total inventory of construction steel continued to decline, and the overall fundamental contradictions are not yet prominent. However, considering the approaching high school and college entrance examinations, some construction sites will be prohibited from operating during specific time periods, and the expectation of weakening demand at the margin still exists. The short-term improvement in sentiment may not be able to sustainably drive up steel prices. Therefore, it is expected that steel inventory may decline next week, but the decline will significantly narrow.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)